In India, the applicable financial year (FY) and assessment year’s income tax slabs and rates are used to calculate income tax. As a part of the Union Budget 2023–24, the income tax slab for AY 2024–25 was released on February 1, 2023.

According to the finance minister, the income tax rebate under the new tax system has been extended from the previous cap of up to Rs. 5 lakh to Rs. 7 lakh. For the new tax regime, there were also some changes to the tax slab. In addition, the surcharge rate on revenue beyond Rs. 5 crore has been lowered from 37% to 25%.

The New Income Tax Portal is now where you can file your taxes. The new interface has a tonne of features and is intended to make tax filing easier.

What is an income tax slab?

Individual taxpayers are required to pay income tax according to the applicable tax slab. Depending on their income, individuals may fit into a different tax bracket. People with higher salaries will thus be required to pay more in taxes. The country’s tax structure was kept equitable by implementing the slab system. With each new budget announcement, the slabs are altered.

Old vs. new tax regime: After the Budget of 2023, which tax system should people choose as their income tax system?

For salaried individuals, senior citizens, and super senior citizens, the break-even point between the previous tax regime and the revised new income tax slabs has been moved by the new tax regime’s revised income tax slabs, which were announced in Budget 2023.

The maximum deduction that must be claimed under the previous tax system in order for the amount of income tax owed under both systems to be equal is referred to as the break-even point here. If a person cannot satisfy a specific amount of deduction, this can assist them in determining which tax system will be preferable for them.

“If the maximum exemptions and deductions claimed by salaried individuals are more than Rs. 4.25 lakh for an income beyond Rs. 15.5 lakh, then he/she may pay less tax in the old tax regime from April 1, 2023,” claims an analysis. A salaried person is automatically eligible for a standard deduction of Rs. 50,000 as part of the exemptions and deductions. To claim the standard deduction, he or she is not obliged to submit any paperwork.

Keep in mind that when calculating the break-even point, the deduction and exemption amounts will fall as the wage levels do as well.

The maximum deductions a salaried person can take to maintain tax neutrality under both income tax systems are shown in the following analysis.

The study shows that the current break-even salary is Rs. 7.5 lakh. In the previous tax system, a person with a salary income of Rs. 7.5 lakh might reduce their taxable income to Rs. 5 lakh by claiming the maximum permitted exemptions and deductions of Rs. 2.5 lakh. As a result, he no longer owes any taxes and is qualified for a rebate under Section 87A of the previous tax code. If the same person chooses the updated new tax regime, they will be eligible for the standard deduction of Rs. 50,000 (introduced for the new tax regime), a Section 87A rebate (for income up to Rs. 7 lakh), and will owe no taxes.

Similarly, if a person with a gross income of Rs. 10 lakh chooses to claim exemptions and deductions such Section 80C, 80D, 80TTA, HRA exemption, and LTA exemption for a maximum of Rs. 3 lakh, then they become tax neutral in both tax systems. For a salaried taxpayer whose claimed deductions are less than Rs. 3 lakh, the new tax system will be advantageous.

The amount of tax payable will be the same under the old tax system and the updated new income tax slabs for salaried individuals with income of Rs. 12.5 lakh who are eligible for deductions (Section 80C, 80D, 80E, 80TTA, etc.), tax exemptions on HRA, LTA, and standard deductions of Rs.50,000 for a maximum total of Rs.3,62,500. It is preferable to choose the revised new income tax system if the amount of the deduction claimed is less than Rs 3,62,000.

To benefit from the old tax system, a salaried person with a gross income of Rs. 15 lakh must deduct more than Rs. 4,08,332 in expenses. For the old tax system to be advantageous, the deductions must total more than Rs. 4,25,000 if the individual has a gross income of Rs. 20 lakh.

Three deductions allowable under the new income tax slabs in 2023 (H1)

By altering its income tax slabs and rates, Budget 2023 has made the new income tax slabs more appealing. In addition, the government has permitted a few deductions that qualified people can use starting on April 1, 2023, under the new tax system.

As of April 1, 2023, the following deductions would be available to qualified persons under the new tax system, according to Budget 2023:

I) The standard deduction for employees, retirees, and family pensioners

ii) The employer’s payment to the employee’s National Pension System (NPS) account is deductible under Section 80CCD (2).

iii) The Agniveer Corpus Fund contribution deduction

“The proposed new tax regime permits a salaried individual to claim the advantage of the basic deduction of Rs. 50,000 and also any NPS contribution by the employer to the employee’s NPS account under Section 80CCD,” says Dr. Suresh Surana, founder of RSM India, a tax consulting firm (2).

Agniveers may additionally deduct their donations to the Agniveer Corpus Fund under the proposed new tax system. Other measures announced to make the new tax system more advantageous for small taxpayers include raising the basic exemption limit to Rs. 3 lakh, increasing the threshold limit of the rebate under the new tax system from Rs. 5 lakh to Rs. 7 lakh of taxable income, reducing the number of tax slabs from 6 to 5, eliminating the 25% tax slab, and capping the surcharge for people with total incomes above Rs. 5 crore at 25% (the previous 37% surcharge was the highest rate). The goal appears to be to encourage the new tax system and raise its level of tax efficiency parity with the prior one.

Here is a closer look at these deductions.

1. Standard deduction

Only taxpayers who earned income during the applicable financial year under the heading “Income from salaries” are eligible for this deduction. Therefore, salaried people and pensioners can only deduct the standard deduction of Rs. 50,000 from their income from wages or pensions.

This deduction may be requested without providing the employer with any supporting documentation. An employer automatically accounts for the standard deduction when calculating taxes on wages.

According to the new tax law, family pensioners are eligible for a standard deduction of Rs 15,000 per year. A family pensioner’s income is taxed under the “Income from other sources” heading.

Based on the budget address, “Only the previous system still permits the standard deduction of Rs 50,000 for salaried individuals and Rs 15,000 for family pension deductions.” It is suggested that the new system also permit these two deductions.”

2. Employer contributions to NPS

As a salaried employee, you are qualified to claim a deduction for the contribution made from gross income if your company makes contributions to your NPS account. According to Section 80CCD (2) of the Income-tax Act of 1961, this deduction is requested.

The maximum amount that an employee may be entitled to under this clause varies depending on whether they work for the government or the private sector. A government employee may deduct a maximum of 14% of their salary, compared to a private sector employee’s maximum deduction of 10% of their pay. Here, salary refers to base pay plus a daily stipend.

Here is an illustration to help you comprehend. Let’s say an employee in the private sector earns an annual base salary of Rs. 8 lakh. Every financial year, his employer contributes Rs 60,000 to the employee’s NPS account. An employee may claim Rs 80,000 (10% of Rs 8 lakh) under Section 80CCD (2). Therefore, the employer’s contribution of Rs 60,000 qualifies for a deduction. However, the employee may only deduct Rs 80,000 if the employer made an annual contribution of Rs 1 lakh.

Keep in mind that if an employer contributes more than Rs 7.5 lakh to the NPS, EPF, and superannuation fund in a fiscal year, the extra contribution will be taxable to the employee. Additionally, any interest or returns received on the surplus donation will also be taxed.

3. Contribution made by Agniveer to Agniveer Corpus Fund

According to Finance Minister Nirmala Sitharaman, Agniveer may deduct any sum paid or deposited to the Agniveer Corpus Fund from income under the recently proposed Section 80CCH of the Income-tax Act.

The Budget 2023 Speech stated that “the Agniveers enrolled in the Agnipath Scheme, 2022, are recommended to receive their payment from the Agniveer Corpus Fund tax-free. It is planned to allow the Agniveer to deduct his or the Central Government’s contribution to his Seva Nidhi account when calculating total income.”

According to the Budget Memorandum, “It is further proposed to insert a new section 80 CCH to the Act to provide that an assessee, being a person enrolled in the Agnipath Scheme and subscribing to the Agniveer Corpus Fund on or after the 1st day of November, 2022, shall be allowed a deduction of the full amount of the amount deposited by him as well as the amount contributed by the Central Government to his account in the Agniveer

Additionally, Agniveer Corpus Fund’s maturity payment is tax-free.

As stated in the Budget Memo, “The Agniveer Corpus Fund is to receive 30% of each Agniveer’s monthly, personalized Agniveer Package.” Additionally, the “Agniveer Corpus Fund” will receive a matching donation from the government. Additionally, the government will give the subscriber interest on the donations that are still in his account, as approved from time to time. Agniveers will receive a one-time “Seva Nidhi” package, which will include their contribution plus interest, as well as a matching contribution from the government equivalent to the total amount of their contribution plus interest, upon completion of the four-year engagement term.”

New Income Tax Regime for FY 2023–2024

The various tables for the FY 2023–2024 revised income tax slabs and rates are shown below:

Individual New Regime Income Tax Slab Rates

Things to consider when choosing a new tax slab

Before choosing the new tax slab, you should bear the following in mind:

If you, as an individual or as a member of a Hindu Undivided Family (HUF), do not have any business income, the option may be exercised on or before January 1 of each year prior.

Once a taxpayer selects the next tax regime as an option, they are unable to change it later in the year. If you change your mind and choose to return to the previous tax system, you can do so again during the current fiscal year.

Income Tax Slab for Individuals Between 60 and 80 Years

Income Tax Slab for Individuals Over 80

Domestic Business Tax Slabs

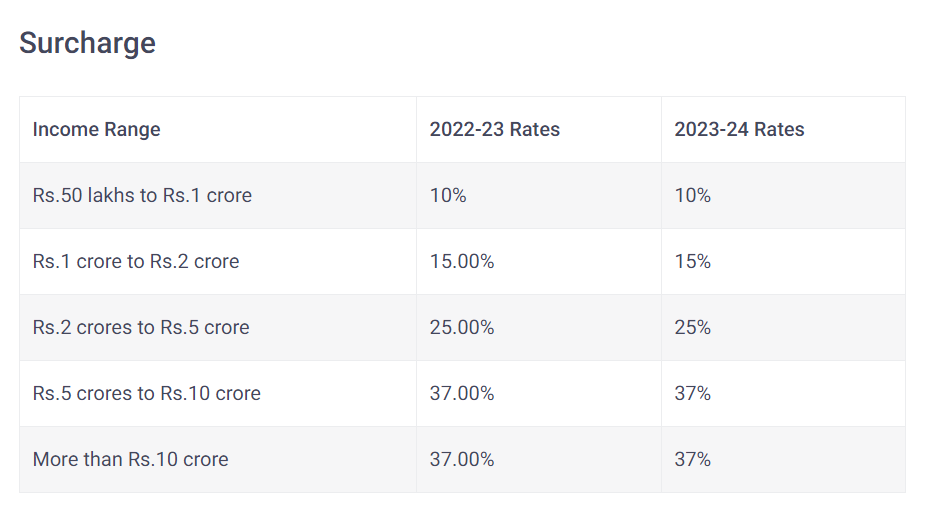

Surcharge-

Taxable Sources of Income in India

Income tax is a law that applies to all individuals, trusts, enterprises, and other types of institutions. As a result, India has a wide range of income sources that are taxable.

Some of the several forms of taxable income in India are listed below:

1. Business Income

Businesses’ profits are included in the calculation of taxable income. The tax in this category is based on any potential income that the profession or business may have, whether that income is assumed or actual. It can only be done once the allowed deductions have been modified.

In the fiscal year 2023–2024, different rates apply to business revenue for corporations and individuals. For the fiscal years 2023–2024, individuals with business income will be subject to income tax rates and slabs.

2. Salary or Pension

The base salary, allowances, and salary profit in this category are frequently taxed. The individual’s pension after retirement is likewise subject to the income tax bracket. Depending on the age of the individual receiving a salary or pension during the fiscal year, different income tax slab rates apply for FY 2023–24.

3. property income

One simple way to increase your income is to own a lot of homes and rent them out. However, in certain situations, rental income from houses is recognised as part of the taxpayer’s income. This income is therefore subject to taxation at the applicable income tax slab rates for the fiscal years 2023–2024.

4. Capital Gains Income

Selling assets like gold, real estate, mutual fund shares, stocks, debentures, and so forth can result in capital gains income. Depending on the type of asset and the long-term earnings generated on it, it can be classified as either a long-term or short-term capital gain.

5. Lottery, Races, and More Income

Winnings from lotteries, horse racing, and other similar events are taxable in India. However, these gains are not included in the income slab rates for the fiscal years 2023–2024 but are instead taxed separately under the present tax code.

Differentiating the Old Regime from the New Regime

In addition to the current tax regime, a new tax regime was put into place for the 2020–21 fiscal year. The new tax system must be used by taxpayers in FY 2023–24 (AY 2024–25), as it was regarded as the default one in FY 23–24. Individuals may still use the previous income tax system, nevertheless. In the new tax system, the government has currently lowered the highest rate surcharge from 37% to 25%.

The two income tax systems in India differ significantly in two ways:

First off, compared to the previous tax system, the new one offers more tax slabs with lower tax rates. As a result, depending on whether you select the new or old tax regime, the income tax slabs for FY 2023–24 change.

Second, if you choose the new tax system, you will no longer be able to take advantage of any of the significant deductions and exemptions that were accessible under the prior tax system, such as Section 80C, Section 80D, and so on.

Tax deductions and exclusions give taxpayers the opportunity to invest, save, or spend money on particular financial instruments while still reducing their tax obligation.

Although the new tax system offers fewer exemptions and deduction options than the old one, the income tax bracket rates for AY 2024–25 are nonetheless higher than under the old system. In contrast, the prior tax code permitted you to exclude up to 70 expenses from your taxable income in order to lower your tax obligation for the fiscal years 2023–2024.

Old vs new income tax regime: Re 1 can cost you Rs25,000 in this tax regime-

New income tax regime: Following the simplification of the new income tax slab and the raising of the Section 87A benefit from 12,500 to 25,000 under both the old and new tax regimes, the salaried middle class is now debating which is more advantageous for them. For middle-class salaried individuals, the budget 2023 pronouncements regarding the income tax exemption on up to Rs 7 lakh in annual income seem appealing, but are they really what they seem?

Finance Minister Nirmala Sitharaman reportedly tried to make the new tax system more appealing by simplifying the new income tax slab and extending the Section 87A advantage to it as well. This is according to tax and investment experts. However, the benefit is not universal because it is only available to those with yearly incomes of up to Rs 7 lakh. If a person earns more than Rs. 7 lakh, then all of their income above Rs. 3 lakh will be subject to income tax.

Balwant Jain, a tax expert based in Mumbai, highlighted the flaw in this old vs. new tax system. “The Section 87A benefit of $25,000 (up from $12,500) announced in this budget has been extended by Finance Minister Nirmala Sitharaman to the new tax system as well. Due to the new income tax slab’s implied taxes of 5% on incomes between 3,00,001 and 6 lakh and 10% on incomes between 6,00,001 and 9 lakh, the 25,000 tax exemption results in zero income tax on income up to 7 lakh under the new income tax regime. The Section 87A benefit will not be available to a taxpayer when they file their income tax return (ITR) if they earn more than $75,000 per year.”

Optima Money Managers’ MD and CEO, Pankaj Mathpal, provided the following explanation of the Section 87A advantage: “The Section 87A benefit, which previously allowed for a tax exemption of $12,500 in a single fiscal year, has now been increased to 12,500 in a single fiscal year. The non-taxable yearly income ceiling has increased from Rs. 5 lakh to Rs. 7 lakh as a result of this exemption. However, if a person earns an annual income of more than Rs. 7 lakh, then they are required to pay income tax on the portion of their income over Rs. 3 lakh.

In contrast to the current income tax regime, Pankaj Mathpal continued, an income tax payer had the option to donate while still being eligible for a tax refund under the previous system. Therefore, starting at 3,000,001, income tax is due if one’s annual income exceeds 75,000 by even just Re 1.

New vs old tax laws

Balwant Jain provided the following explanation of how a taxpayer’s Re 1 income could turn into a nightmare: “If a person makes $7,00,006 in a fiscal year, as $7,00,005 would be considered $7 lakh in annual income, there would be a 5% tax on earnings between $3,00,001 and $6 lakh and a 10% tax on earnings between $6,00,01 and $7,00,005. This translates to a tax of $15,000 on income between $3,000 and $6 lakh and a tax of $10,000 on income between $6,000 and $7,00,005. Therefore, the extra Re 1 may result in an additional 25,000 in income tax expenses under the new tax system, which a taxpayer can avoid by using the donation option allowed under the previous system.”

Tax rebate under Income-tax Act Section 87A?

According to the adjustments made in the new tax system revealed in the Budget 2023, a person will not be required to pay taxes if their taxable income does not exceed Rs 7 lakh in a financial year. Salaried people and other taxpayers should not confuse this with the fundamental exemption cap under the new tax system, however.

The basic exemption threshold was increased in the Budget 2023 from Rs 2.5 lakh to Rs 3 lakh. As a result, if a person’s income reaches Rs 3 lakh during a financial year, it becomes taxable. To reiterate, under the new tax system, no tax is due if the taxable income is less than Rs 7 lakh.

This advantage results from the tax credit provided by Section 87A of the Income-tax Act of 1961.

Who is eligible for a Section 87A tax rebate?

The rebate under Section 87A is exclusively available to residents, according to the Income-tax Act. Non-resident taxpayers (NRIs), Hindu undivided families (HUFs), and businesses are not qualified for the rebate under Section 87A.

How much tax relief is provided under Section 87A?

Both the previous and new tax regimes, as well as the tax refund, are applicable. The amount of the tax rebate accessible under both tax regimes would remain the same through FY 2022–2023. If their taxable income does not exceed Rs 5 lakh in a financial year, anyone choosing the new tax regime for any financial year up until FY 2022–23 (ending on March 31, 2023) will be eligible for a tax rebate of Rs 12,500. Similarly, even under the previous tax system, taxpayers with taxable income up to Rs 5 lakh were eligible for a tax credit of Rs 12,500.

In the previous tax system, the taxable income was determined after all tax deductions and exemptions were claimed. Common deductions and exclusions are not permitted under the new tax system until FY 2022–2023

However, the tax rebate amount accessible under the new tax system beginning in FY 2023–24 has increased. This is as a result of the government updating the income tax slabs for the new tax system beginning in FY 2023–2024.

The rebate under Section 87A has been increased to Rs 25,000 for taxable income up to Rs 7 lakh in order to make the new tax system more enticing. As a result, if their taxable income is less than Rs 7 lakh, a person choosing the new tax system in FY 2023–24 will pay no taxes.

The Section 87A tax rebate that was previously offered for FY 2023–2024 has remained unchanged.

How can I submit a Section 87A tax rebate claim?

Depending on the income tax system you choose, there are certain steps to claim a tax rebate under Section 87A.

Step 1: Determine your gross annual income from all sources if you are choosing the new tax system.

Step 2: After the calculation, take all the deductions you are entitled to. An individual is qualified for the employer’s payment to the employee’s NPS account under Section 80CCD (2) in FY 2022–2023. A salaried employee would also be qualified for a standard deduction of Rs 50,000 starting in the fiscal year 2023–24.

Step 3: You obtain the net taxable income by subtracting the deductions from the gross taxable income. You are entitled to the tax credit under Section 87A if your net taxable income is less than Rs 7 lakh. At the time the income tax return is filed, this rebate will automatically be taken into consideration. The tax payable will be shown as 0.

If you choose the old tax system

Step 1: Determine your overall gross revenue from all sources.

Step 2: After the calculation, take all the deductions you are entitled to. The former tax system’s income tax rates and slabs are remaining unchanged. Therefore, a person is eligible to claim all tax benefits, including HRA, LTA, and deductions under Sections 80C and 80D, among others.

Step 3: One obtains the net taxable income by subtracting the deductions from the gross taxable income. You qualify for the Section 87A tax credit if your net taxable income is less than Rs 5 lakh. When completing an income tax return, the tax rebate will be automatically taken into account. The tax payable will be shown as 0.

FAQs- (H2)

1. How is the income of a taxpayer classified?

According to Section 14 of the Income Tax Act, the taxpayer’s income has been categorised into five different income heads, including Individual Salaries, Capital Gains, Profits from a Profession or a Business, Income from Home, and Income from Other Sources.

2. If my annual income is less than Rs. 2.5 lakh, do I still need to file an income tax return?

If your yearly income is under Rs. 2.5 lakh, you are not required to submit an ITR; nonetheless, you must file a “Nil Return” only for record-keeping purposes because you can use it as evidence of employment in various situations.

3. Who qualifies for financial assistance under Section 87A?

Any resident of India who earns less than Rs. 5 lakh annually may be eligible for a rebate under Section 87A. Section 87A allows for a maximum reimbursement of Rs. 12,500.

4. When will suggestions for changes to India’s income tax brackets be made?

India’s finance minister makes the announcements regarding changes to the income tax brackets in that nation. This recommendation is often made in February each year, when the annual budget is unveiled.

5. Does a family pension qualify as a salary for tax purposes?

No, a family pension is taxed as “income from other sources,” not as salary income.

6. If I work in agriculture, is my income subject to taxation?

Agriculture and its related industries do not subject any income to taxation. However, it will be taken into account for determining your tax rate for any non-agricultural income you may have.

7. Is income up to Rs. 5 lakh tax-free?

No, income up to Rs. 5 lakh is not exempt from tax. However, under the new system, people who earn up to Rs. 3 lakh are exempt from paying taxes.

8. Can I change my tax filing’s income tax regime?

Yes, depending on your preferences, you can opt to file your income tax returns under the old regime or the new regime.

9. Are India’s income tax brackets subject to change?

Yes, there may be modifications to India’s income tax rates.

10. Who alters the income tax rates in India?

The Finance Ministry of India has made adjustments to the income tax brackets in India.

11. Has the Budget of 2023 made any modifications to the existing tax system?

The former tax system’s income tax rates and slabs have not changed as of Budget 2023.

12. What is the basic exemption limit for the new tax system for the fiscal years 2023–2024?

Beginning on April 1, 2023, the basic income exemption threshold will be Rs 3 lakh. In the budget for 2023, this ceiling was increased from Rs 2.5 lakh.

13. Can you deduct anything under the new tax system in 2023?

For salaried individuals and retirees, the standard deduction in the Budget 2023 is Rs. 50,000. In addition, they may deduct some expenses under Section 80CCD (2) of the Income-tax Act of 1961.

14. What are the surcharge rates under the new tax system for the fiscal years 2023–2024?

According to the new tax system proposed by the government for FY 2023–2024, the surcharge rate will be adjusted. the following updated surcharge rate: (A) 10% of taxable income in excess of Rs. 50 lakh (B) Above Rs. 1 crore, there is a 15% tax rate; above Rs. 2 crore, there is a 25% tax rate.

15. What does the new tax system’s Section 87A tax rebate involve?

Under the new tax law, there is a 25,000-rupee tax credit available. This tax credit is available to all individuals with an annual taxable income of less than Rs 7 lakh. As a result, the effective tax outgo would be zero.